Amid An Uphill Payer Innovation Battle, Enhabit Announces New MA, Leave a comment

Enhabit Inc. (NYSE: EHAB) is soon to be one of the only independent home health companies remaining on the public market. And its struggle to turn its business into a Medicare Advantage-friendly one – on the fly – is something the entire industry will be paying attention to.

Barb Jacobsmeyer, Enhabit’s CEO, has tried to emphasize the importance of the transformation that the company is currently undertaking.

In essence, before it could even find its footing on the public market, it needed to upheave its operations to get more – and better – MA contracts and adjust to a workforce more comprised of part-time workers.

That effort is still ongoing. And while it may be a valiant and worthwhile one, earnings aren’t generally boosted due to those factors.

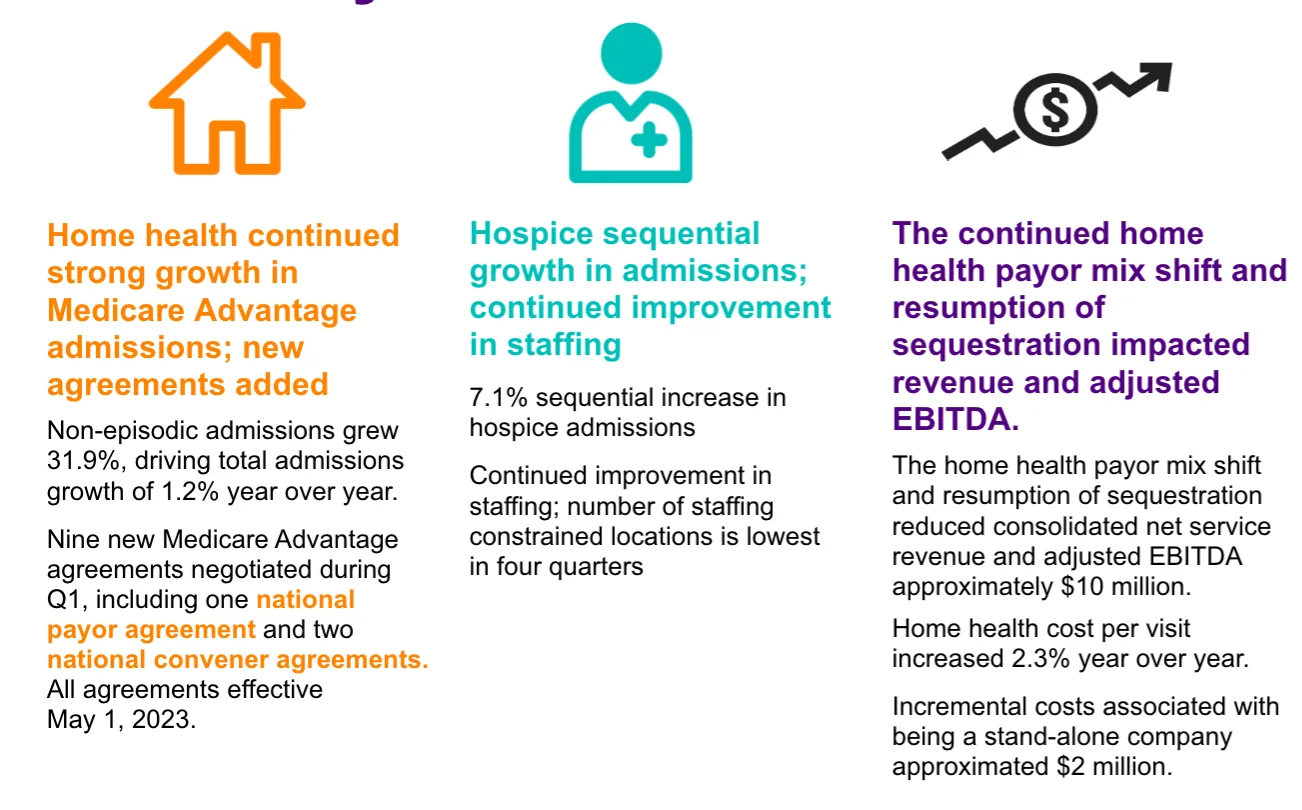

“We continue to make progress in two of our critical success factors for 2023 – payer innovation and the recruitment and retention of clinical staff,” Jacobsmeyer said Wednesday on the company’s first-quarter earnings call.

Amid these adjustments, Enhabit is still taking stock of its wins. The company has put its foot down with certain MA plans, prioritizing the payer sources that pay fairly for home health services.

“The most significant update is our executed agreement with a national payer that became effective May 1, and our branches are excited and ready to accept these patients that they historically had to decline,” Jacobsmeyer said.

Enhabit did not specify which payer it has entered into an agreement with. But, in addition, the company announced that it had signed two agreements with conveners that had national reach.

Conveners – which often draw ire from home health providers for suppressing payment – are generally the middlemen between MA plans and home health providers. They help control post-acute spend and utilization, often creating a network of providers on behalf of the plan to do so.

The agreements with the two unnamed conveners also became effective on May 1.

“We look forward to working alongside these conveners to solve challenges and deliver accessibility for patients in home-based care,” Jacobsmeyer said.

Jacobsmeyer seemed to suggest that at least some conveners are beginning to recognize the need for consistent and high-quality home health provider partners.

Each quarter, Enhabit leaders have announced new agreements with payers – at the regional level, at the national level and now with conveners.

Part of that process has also been internal. The corporate office has had to sit down with the company’s branch locations to explain why the company can no longer to afford to take on certain patients, and instead has to prioritize specific plan partners or Medicare fee-for-service patients.

“To date, we have visited branch operations and sales teams covering 159 branches,” Jacobsmeyer said. “We believe it’s important to take time to sit down and be transparent as we present not only how, but why, we must be select certain payers and replace them with the new regional and national agreements.”

While acknowledging that a patient is on the other side of these decisions, she emphasized that without prioritizing certain payer sources, the company’s ability to reinvest in its “people and technologies” is jeopardized.

In the first quarter, net service revenue totaled $265.1 million for Enhabit, a 3.4% year-over-year decrease. Home health revenue accounted for $216 million of that, and also decreased by 4% year over year.

Home health episodic admissions checked in at 35,032 for the quarter, a 10.1% year-over-year decrease. At the same time, non-episodic admissions grew to 18,911, a 31.9% year-over-year increase.

Source: Enhabit

Source: Enhabit

Still, episodic admissions increased sequentially for the first time since Q1 of 2022, mostly driven by new MA contracts that pay episodically, Enhabit CFO Crissy Carlisle said on the call.

To put the overarching transformation into perspective, Carlisle laid out some numbers.

“Every 5% of current non-episodic visits under one of our historic contracts that we can move to one of these new national or regional contracts, that’s worth $2 million of adjusted EBITDA annually,” she said.

Based on the newness of some of these contracts, it will take time for those millions to materialize.

Other headwinds, tailwinds

Despite the more regular conversation around MA, the looming home health proposed payment rule for traditional Medicare is not lost on Enhabit leaders. Jacobsmeyer, in fact, laid out some predictions for it.

“I don’t think that we would be surprised to see the other half of that behavioral adjustment come through,” she said. “I think we will be surprised if they propose to implement any temporary cuts [on top of that].”

Enhabit leaders also believe that the staffing situation is improving and that, over time, there will be less locations in the company’s network that are constrained.

Over 100 new full-time nurses were hired in the first quarter – 91 in home health and 10 in hospice.

It’s fair to wonder if a “deep-pocketed partner,” as one analyst put it, is in the future for Enhabit given the recent news that Amedisys Inc. (Nasdaq: AMED) plans to combine with Option Care Health (Nasdaq: OPCH).

Carlisle reiterated, however, that the company’s focus remains on payer innovation and solving the staffing situation.

“I think it’s difficult to speculate on various announcements and transactions in the industry,” she said. “We are focused on operating this company and executing on our payer innovation strategy, as well as our recruitment and retention strategy. That’s really all we can say.”